Odie Pet Insurance at a Glance

- Odie Pet Insurance was founded in 2020 by Miles and Zabrina Thorson, two dog owners with over 30 years of combined insurance experience, and was built specifically to address the affordability gap in pet health coverage.

- Odie offers customizable accident and illness plans, an accident-only option, and optional wellness add-ons with no upper age limit for enrollment.

- Claims are typically paid out within five days, but Odie has received low customer ratings on BBB and Trustpilot — a detail worth knowing before you sign up.

- Odie’s annual limit maxes out at $40,000, which puts it behind competitors that offer up to $100,000 — a real consideration for high-cost breeds or complex conditions.

- Keep reading to find out exactly who Odie is right for, where it falls short, and how it stacks up against top competitors in 2026.

If you’re weighing whether Odie Pet Insurance is worth your money in 2026, the short answer is: it depends entirely on what you need from a policy.

Pet insurance has gone from a niche product to a near-essential financial tool for dog owners — and with hundreds of thousands of pets now insured across the U.S., the competition between providers has never been fiercer. Odie entered the market in 2020 with a clear value proposition: flexible, affordable coverage with no age limits and fast claim payouts. For budget-conscious pet owners, that combination is genuinely attractive.

But affordability alone doesn’t make a policy worth buying. Coverage gaps, waiting periods, and customer service track records all matter — sometimes more than the monthly premium. This review breaks down everything you need to know about Odie in 2026, from what’s actually covered to how it compares against stronger competitors.

Odie Pet Insurance: The Fast Facts Dog Owners Need

Odie is a California-based pet insurance company that has been covering dogs and cats nationwide since 2020. It’s one of the newer players in a crowded space, but it has carved out a niche by offering customizable, low-cost plans that work for a wide range of pet owners — from those insuring puppies to senior dogs with no upper age limit.

Founded in 2020 by Two Dog Owners With Insurance Expertise

Miles Thorson and Zabrina Thorson co-founded Odie after recognizing a gap in the market for pet insurance that was both genuinely affordable and flexible enough to fit different budgets. With more than three decades of combined insurance industry experience between them, the Thorsons built Odie from the ground up to make quality coverage accessible. That origin story matters because it shaped how Odie structures its plans — prioritizing customization and price over one-size-fits-all coverage tiers.

Available in All 50 U.S. States

Odie is available nationwide, including travel coverage that extends to Canada and Puerto Rico. That’s a meaningful perk for dog owners who travel frequently or split time between locations. You can use any licensed veterinarian in your state, which means you’re not locked into a network — a flexibility point that not every competitor offers.

Scored 4.2 Out of 5 Stars in Independent Methodology Testing

In independent review methodology scoring, Odie has earned a 4.2 out of 5 stars — a solid result for a company only a few years old. However, customer-facing ratings tell a different story. Odie currently holds a 1-star rating on the Better Business Bureau and a 2.2-star rating on Trustpilot. That gap between methodology scores and real customer experiences is something to factor carefully into your decision.

What Odie Pet Insurance Actually Covers

Odie’s coverage breaks down into two core plan types — accident and illness, and accident-only — plus optional wellness add-ons. Understanding exactly what falls inside and outside those plans is the most important part of evaluating whether Odie is right for your dog.

Accident and Illness Plan: What’s Included

Odie’s flagship plan covers a broad range of medical situations. Here’s what’s included under the accident and illness plan:

- Accidental injuries (fractures, lacerations, swallowed objects)

- Illnesses, including infections, cancer, and diabetes

- Genetic and hereditary conditions

- Specialist and emergency vet care

- Diagnostic tests, imaging, and bloodwork

- Surgeries and hospitalization

- Prescription medications

- Chronic condition management

Coverage for hereditary and genetic conditions is a standout feature — many budget pet insurance providers exclude these entirely, which can be a costly oversight for purebred dog owners prone to breed-specific conditions like hip dysplasia in German Shepherds or heart disease in Cavalier King Charles Spaniels.

Accident-Only Plan: Who It’s Best For

The accident-only plan is Odie’s most affordable entry point. It covers injuries from unexpected events — think broken bones, bite wounds, or toxic ingestion — but excludes illness coverage entirely. This plan suits owners of young, healthy dogs who want a financial safety net for emergencies without paying for full illness coverage they may not need yet.

Optional Add-Ons That Boost Your Coverage

Odie offers wellness plan add-ons that go beyond what standard accident and illness policies include. These optional riders cover routine and preventative care, such as annual exams, vaccinations, flea and tick prevention, and dental cleanings. Adding a wellness plan transforms Odie from a reactive coverage tool into something closer to a comprehensive pet health management solution — though the added cost needs to be weighed against what you’d actually use.

What Odie Does Not Cover

Like every pet insurance provider, Odie has exclusions. The most important ones to know upfront:

- Pre-existing conditions (conditions that existed before your policy start date)

- Cosmetic procedures

- Breeding costs and pregnancy

- Elective surgeries

- Experimental treatments

Pre-existing condition exclusions are standard across the industry, but they’re especially worth noting if you’re enrolling an older dog or one with a documented health history. Waiting periods also apply before coverage kicks in — which leads directly into the cost and timing details below.

Get Your Quote By Clicking Here

How Much Does Odie Pet Insurance Cost for Dogs

Odie’s pricing is one of its strongest selling points. Monthly premiums vary based on your dog’s age, breed, species, and ZIP code, but Odie consistently positions itself among the more affordable options on the market. That said, “affordable” looks different depending on how you configure your policy — and the customization options Odie offers give you real control over what you pay each month.

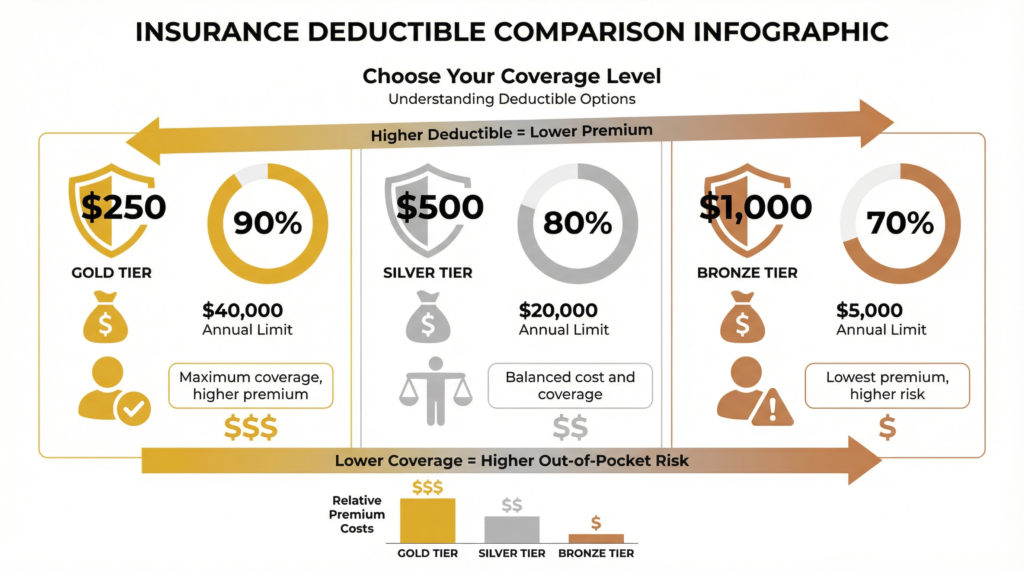

Deductible, Reimbursement, and Annual Limit Options

Odie gives you three key levers to adjust your monthly premium: your annual deductible, your reimbursement percentage, and your annual limit. Deductibles range from $250 to $1,000 — the higher you set it, the lower your monthly cost. Reimbursement rates sit at 70%, 80%, or 90%, meaning Odie covers that percentage of eligible vet bills after your deductible is met. Annual limits range from $5,000 to $40,000, offering budget-conscious owners flexibility but falling short of competitors that offer $100,000 or unlimited annual limits.

5% Multi-Pet Discount and Other Ways to Save

If you have more than one pet, Odie offers a 5% multi-pet discount — a straightforward saving that adds up over a 12-month policy year. It’s not the deepest discount in the industry, but it’s a consistent perk for multi-dog households.

Beyond the multi-pet discount, the most effective way to lower your Odie premium is to raise your deductible and lower your reimbursement rate. Setting a $1,000 deductible with a 70% reimbursement rate will produce the lowest monthly premium, though it means more out-of-pocket cost when you actually file a claim. Finding the right balance between premium and out-of-pocket risk is the core financial decision every pet owner needs to make before selecting a plan tier.

Keep in mind that your pet’s age and breed will influence which configuration actually makes financial sense. A three-year-old mixed breed in a low-cost-of-living state will look very different on paper compared to a six-year-old French Bulldog in California — a breed notoriously prone to respiratory, spinal, and skin conditions that generate significant vet bills.

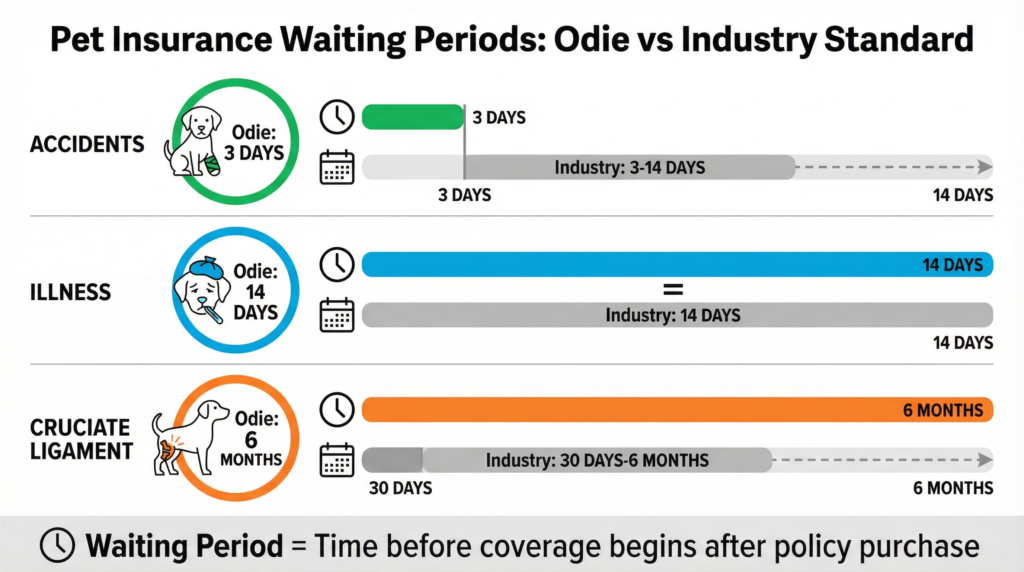

Odie Waiting Periods Dog Owners Should Know

Waiting periods are the gap between when your policy starts and when your coverage actually kicks in. Every pet insurance provider has them — they exist to prevent owners from signing up right before a known vet visit and immediately filing a claim. Odie’s waiting periods are mostly in line with industry standards, with one notable exception that dog owners need to pay close attention to.

For accident coverage, Odie imposes a three-day waiting period — meaning you’re covered for injuries starting on day four of your policy. Illness coverage has a 14-day waiting period, which is standard across most providers. These timeframes are manageable and shouldn’t be a dealbreaker for most owners who are planning ahead rather than reacting to an existing problem.

Where Odie stands out — and not in a good way — is its cruciate ligament waiting period. Odie requires a six-month waiting period before cruciate ligament injuries are covered. This is significantly longer than what many competitors impose and is a critical detail for owners of larger breeds like Labrador Retrievers, Rottweilers, and Golden Retrievers, which are statistically more prone to cruciate ligament tears.

Six-Month Cruciate Ligament Waiting Period vs. Industry Standard

A cruciate ligament surgery for a dog can cost anywhere from $3,500 to $7,000 per leg, making it one of the most financially devastating orthopedic injuries a dog owner can face. Waiting six months for that coverage to activate means you’re carrying significant financial risk during that window. If your large-breed dog tears a cruciate ligament in month three of your policy, you’re paying the entire bill out of pocket. For owners of high-risk breeds, this waiting period alone may be reason enough to look at competitors with shorter windows.

Odie’s Wellness Plan: Is Preventive Coverage Worth Adding?

Odie’s optional wellness add-on covers the routine care that standard accident and illness plans skip entirely — annual wellness exams, core and non-core vaccinations, flea, tick, and heartworm prevention, and dental cleanings. For dog owners who already spend consistently on preventive care each year, a wellness rider can effectively turn those predictable expenses into covered line items. The value equation is simple: add up what you spend annually on routine vet visits and prevention, then compare that to the add-on cost. If your routine spending exceeds the rider premium, it’s worth it. If your dog is young and healthy with minimal preventative needs, the math may not work in your favor.

How Odie Handles Claims and Payouts

The claims process is where pet insurance companies either earn or lose their customers’ trust. Odie’s system is straightforward — you pay your vet bill upfront, submit a claim through Odie’s website, and wait for reimbursement. The absence of direct vet payment means you need to have the funds available to cover a bill before you see any money back, which is worth factoring into your financial planning.

Five-Day Claim Payout Timeframe

Odie advertises a five-day claim payout window — meaning once your claim is approved, you can expect reimbursement within five business days. That’s faster than many competitors in the space and is one of Odie’s most frequently praised operational features. For owners dealing with a large unexpected vet bill, a five-day turnaround versus a 10-to-30-day wait from other providers is a meaningful difference in cash flow management.

Direct Deposit vs. Check Reimbursement

Odie offers two reimbursement methods: direct deposit to your bank account or a traditional check by mail. Direct deposit is the faster option, and the one most owners will prefer — particularly given the five-day payout promise. Choosing check reimbursement adds mail delivery time to the processing window, which can push your actual receipt of funds well past that five-day benchmark.

No Mobile App: Filing Claims Through the Website Only

Important Note for Tech-Forward Pet Owners: Odie does not currently offer a dedicated mobile app. All claim submissions, policy management, and account access are handled through the Odie website. If a streamlined mobile experience is important to you, this is a genuine limitation compared to competitors like Nationwide or Trupanion, which offer app-based claim filing and policy tracking.

The lack of a mobile app is a usability gap that feels increasingly significant in 2026, when most financial and insurance products have moved to mobile-first experiences. Filing a claim from an emergency vet’s waiting room via a mobile browser is doable, but it’s a friction point that a dedicated app would eliminate.

That said, Odie offers 24/7 access to a vet hotline — a feature that partially compensates for the app gap by giving owners immediate professional guidance without going through the claims portal. The hotline lets you speak with a licensed veterinarian at any hour, which is particularly valuable for late-night health concerns that may or may not warrant a costly emergency vet visit.

Overall, Odie’s claims process is functional and faster than average on paper, but the website-only submission model and the requirement to pay upfront mean it works best for owners who are organized, financially prepared, and comfortable navigating a desktop or mobile browser interface when stress is running high.

Odie Pet Insurance vs. Top Competitors

Odie competes in a crowded market against well-established providers with deeper resources, longer track records, and in some cases, significantly broader coverage options. Where Odie wins is almost always on price. Where it loses is typically on annual limits, customer satisfaction ratings, and features like mobile apps or direct vet payment. Understanding those trade-offs is essential before committing to a policy.

The table below shows how Odie stacks up against key competitors on the metrics that matter most to dog owners making a coverage decision in 2026.

Odie vs. GEICO Pet Insurance: Coverage Gaps to Know

When comparing Odie directly to GEICO Pet Insurance — which partners with third-party underwriters to offer its policies — the most notable difference is in the annual limit ceiling. GEICO’s pet insurance offerings can reach up to $100,000 in annual coverage, more than double Odie’s $40,000 maximum. For owners of large or high-risk breeds where a single orthopedic surgery, cancer treatment, or chronic condition management plan could run $15,000 to $30,000 or more in a single policy year, that $60,000 gap in maximum coverage is not a minor distinction — it’s the difference between being fully protected and being underinsured when it matters most.

Where Odie Wins on Price

Odie’s monthly premiums are consistently lower than most mid-tier and premium competitors. For owners of young, healthy mixed-breed dogs in lower-cost-of-living states, Odie can deliver solid accident and illness coverage at a price point that makes financial sense — especially when configured with a higher deductible and a moderate reimbursement rate. The no-upper-age-limit policy also means senior dog owners who get priced out or flatly rejected by other providers have a real option with Odie.

Where Odie Falls Short Against Rivals

The $40,000 annual limit ceiling is the single biggest structural weakness in Odie’s offering. Cancer treatment for dogs — one of the most common reasons pet owners file large claims — can easily exceed $10,000 to $20,000 for chemotherapy, radiation, and surgery combined. Add a second major condition in the same policy year, and you can see how a $40,000 cap gets consumed faster than most owners anticipate. Beyond limits, the low BBB and Trustpilot ratings signal real customer experience issues that go beyond isolated complaints. And without a mobile app, Odie simply doesn’t meet the convenience standard set by competitors like Trupanion and Lemonade.

Who Should Buy Odie Pet Insurance in 2026?

Odie makes the most sense for a specific type of pet owner. If you have a young, generally healthy dog, you’re working with a tight monthly budget, and you want basic financial protection against unexpected accidents and illnesses without paying for premium-tier features you may never use, Odie is a legitimate option worth getting a quote on. The no-age-limit enrollment is also a genuine differentiator for owners of senior dogs who need coverage but keep hitting rejection walls with other providers.

Odie is a harder sell for owners of large-breed dogs prone to orthopedic injuries, purebred dogs with known hereditary condition risks, or anyone whose dog has already been diagnosed with a condition that could escalate into five-figure treatment costs. In those situations, the $40,000 annual cap and the six-month cruciate ligament waiting period create coverage gaps that could cost you significantly more than the premium savings are worth. The right fit for Odie is a budget-first, lower-risk dog owner — not a high-need medical pet household.

Is Odie Pet Insurance Worth It for Dog Owners?

Odie Pet Insurance is worth it if price is your primary driver and your dog doesn’t fall into a high-risk category. It delivers real, customizable coverage at competitive monthly rates, pays claims faster than most plans, and removes the age barrier that keeps senior dog owners out of other plans. But if you’re looking for the highest annual limits, the best customer satisfaction ratings, or a seamless mobile claims experience, there are stronger options on the market in 2026. Odie earns its place as a budget-tier provider — just go in with clear eyes about what the $40,000 limit and six-month cruciate waiting period actually mean for your specific dog’s risk profile.

Frequently Asked Questions

Does Odie Pet Insurance Cover Preexisting Conditions?

No — Odie does not cover preexisting conditions. A preexisting condition is any illness, injury, or symptom that existed before your policy’s effective start date, including conditions your dog showed signs of during the waiting period. This is standard practice across the pet insurance industry and is not unique to Odie, but it makes timing your enrollment critically important. The earlier you enroll your dog — ideally while they’re young and healthy with no documented health history — the fewer conditions are likely to be classified as preexisting and excluded from your coverage.

Is There an Age Restriction for Dogs on Odie’s Plans?

No. Odie has no upper age limit for enrollment, which sets it apart from many competitors that cap enrollment at 8 or 10 years old. This is one of Odie’s most meaningful policy features for owners of older dogs who are often left with few or no options as their pets age into higher-risk health territory.

That said, while there’s no hard age cutoff, premiums do increase with age — as they do with every pet insurance provider. An eight-year-old Labrador will cost significantly more to insure than a two-year-old of the same breed, regardless of which provider you use. The no-age-limit policy means you can get coverage, but the cost of coverage does not stay flat as your dog gets older.

Can I Use Any Vet With Odie Pet Insurance?

Yes. Odie operates on a reimbursement model that lets you use any licensed veterinarian in the United States. You are not restricted to an in-network provider list, which means you can continue seeing your existing vet, visit a specialist, or use an emergency animal hospital and still be eligible for reimbursement on covered expenses.

The reimbursement model requires you to pay your vet bill upfront and then submit a claim for reimbursement afterward. This is the standard operating model for most U.S. pet insurance providers — true direct-pay arrangements where the insurer pays the vet directly are rare. Make sure you have a financial buffer available to cover unexpected vet bills in full before reimbursement arrives, even with Odie’s relatively fast five-day payout window.

What Is Odie’s 30-Day Free-Look Period?

Odie offers a 30-day free-look period, which means you can cancel your policy within the first 30 days for a full refund — as long as you haven’t filed a claim during that time. This is a consumer-protection feature that gives new policyholders a genuine trial window to review the full terms and conditions of their policy after purchase.

Use the 30-day free-look period intentionally. Read through your policy documents carefully during this window, paying specific attention to the exclusions list, waiting period timelines, and how your chosen deductible and reimbursement rate interact with your annual limit. If anything doesn’t align with what you expected when you bought the policy, this is your no-risk exit opportunity.

Does Odie Pet Insurance Cover Prescription Medications for Dogs?

Yes — prescription medications are covered under Odie’s accident and illness plan when they are prescribed to treat a covered condition. This includes medications related to infections, chronic illness management, post-surgical recovery, and other medically necessary treatments that fall within the scope of your policy.

Medications prescribed to treat a preexisting condition, however, are not covered. If your dog was already on a long-term prescription before your policy started — for allergies, thyroid disease, or joint pain, for example — those ongoing medication costs will not be reimbursable through Odie.

Routine flea, tick, and heartworm prevention medications are not covered under the standard accident and illness plan. These fall under preventative care and are only reimbursable if you’ve added a wellness plan rider to your base policy. If your annual prevention spending is a meaningful budget line, the wellness add-on may be worth pricing out to see whether it covers enough of that cost to justify the additional monthly premium.

Get Your Quote By Clicking Here

Leave a Reply